Following Fed Chair Jerome Powell’s Jackson Hole speech, markets are taking a short breather with higher hopes of a September rate cut. Both big tech and small cap are in the spotlight, but where should investors focus?

While lower rates could provide a tailwind for small caps, we still see tech as leadership.

Is it overbought? Maybe. But we remain overweight in tech because we’re investing with a long-term lens.

Hear more insights in Brooke’s Bloomberg interview below. 👇

Transcript:

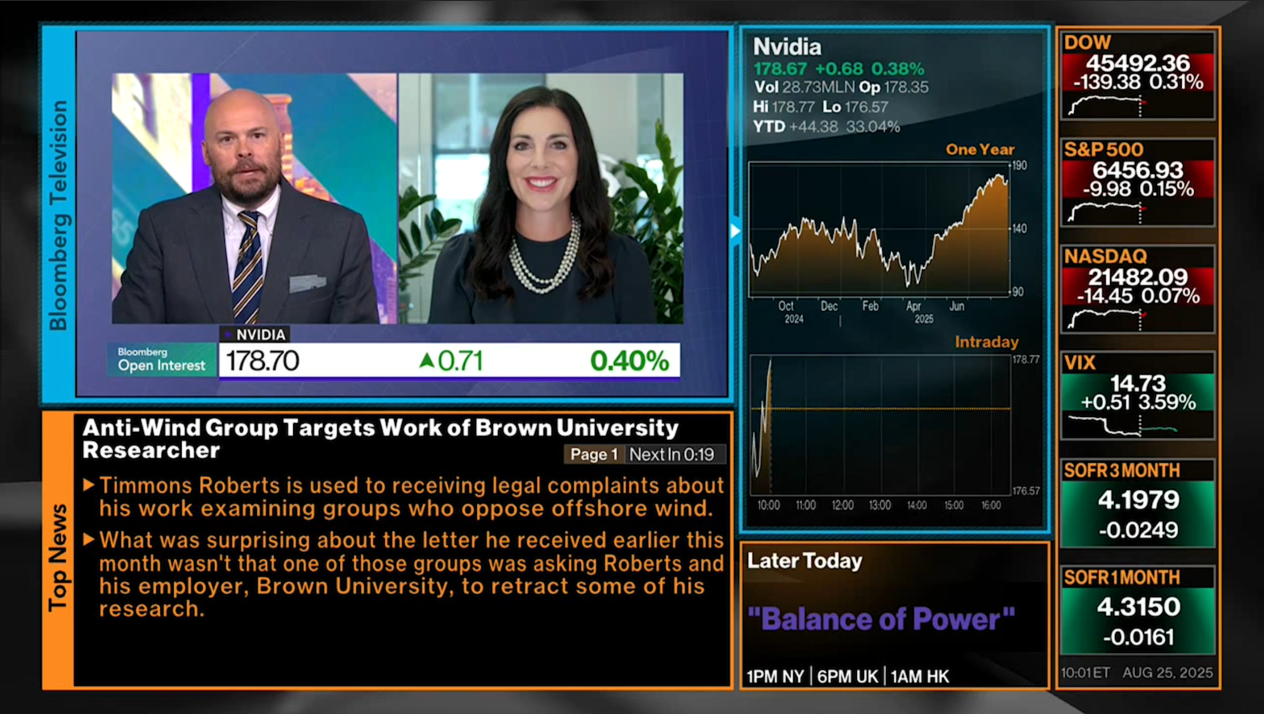

The stocks that we’re watching. Well, the biggest stock that we’re watching and the biggest stock in the world is Nvidia. It accounts for 3% of the world’s total market capitalization. Shares are expected to move more than 5% in either direction after the report on Wednesday.

Evans May Wealth managing partner Brooke May joins us now. I’m giving the implied move. That doesn’t mean it’s going to happen. That’s just based on what we’ve seen in the past.

What do you think about Nvidia earnings? How important is this event?

They’re massively important. As you alluded to, they have significant weighting globally, but especially in the S&P 500 and Nvidia has a great history of beating on earnings expectations.

But guidance is going to mean a lot. 58% of companies raised their guidance in Q2, and we expect the same out of Nvidia. If we don’t get it, then we’ll see some volatility in the market.

What does that volatility look like? Because we’ve already had tech stocks falling before Friday. They had fallen for five consecutive days.

How vulnerable or resilient is this market to a bad print from Nvidia?

I think that it could lead to some volatility to the tune of 5% or 3%. Who knows? It depends on how bad guidance would be, which isn’t necessarily our base case, but it could be a catalyst to create some volatility. When we look at Nvidia, they are the leadership.

We think that we’re in a megatrend for technology. And Nvidia is leading the way. That said, a lot of tech companies are signaling to be overbought. And we wouldn’t be surprised if we see a modest sell-off if Nvidia disappoints.

This company, though, has just grown so quickly in the Mag 7—or Mag 8, if you want to include Broadcom. It has just taken so much of the concentration of the S&P 500.

How are you advising your clients in this kind of situation to rebalance? Do you just set it and forget it once a year, or do you have to rebalance every quarter? How does it work?

We make tactical shifts. For example, we added gold earlier in the year. It’s based on the current environment and the data that we’re getting. But we make tweaks. We don’t get in and out of the market.

We do believe, though, that we are in a megatrend for technology. So, we like the overweight of technology in our portfolios. Nvidia is one of our biggest holdings, if not the biggest in our growth strategy. And so, we think that you still have to be overweight in tech and just take on a little bit of volatility if we see some disappointment here and there. But overall, we think over the next six months, one year, 18 months, technology is going to continue to be leadership.

Well, tech hasn’t been the only thing doing well as of very recently. On Friday, after we had Powell, who very much so opened the door for a September rate cut, you saw small caps up 3.9%. We were just speaking with Keith who upgraded his view on small caps.

Can you get the rest of the market broadening out alongside tech, continuing to rally?

I wouldn’t be surprised if we see a very short-term rally in small cap. However, we’re still underweight. We think that yes, lower rates will help small cap companies because they do have a lot of debt, and a lot of their debt is variable. So lower rates will clearly have an impact on earnings in a positive way. However, they’re smaller companies. They don’t have the ability and leverage to negotiate really hard with suppliers.

And that’s needed right now with higher input costs. In addition to that, capital expenditures have a little bit more of an impact with smaller companies. And if they need to upgrade their technology or implement more AI, it can be a little bit more of a burden to earnings. So, we like large cap right now over small cap.

And we’ll probably continue to have an underweight there until we clearly see that we’re going to have rate cuts materialize.

What’s on your risk checklist here? What would make you more defensive than wanting to buy dips?

The labor market. Everything is hinging on the labor market. When we look back over the last few years, a lot of strategists were calling for a recession, and it hasn’t materialized because of the labor market.

We’ve seen unemployment at 4% to 4.2% since May of 2024. And that’s a really healthy labor market. Right now, the Fed’s indicating that they think unemployment could go to 4.5% over the next year, which would be a tick up. And in the near term, as we see those tenths or two-tenths of a percent raise, it could lead to some volatility, but it isn’t necessarily going to lead to a recession.

In fact, if you listen to earnings calls, only 4% of earnings calls use the word “recession”. In addition to that, in the most recent CEO survey, two-thirds don’t think that we’ll see a recession over the next 12 months. So, we think that, really, it’s all data dependent. And we think that the labor market right now is the biggest risk.

Well, speaking of earnings, you noted that 58% of companies increased their full year guidance, showing that maybe the impact of tariffs wasn’t as severe as we thought. But we also heard from Walmart last week saying every single week the cost of products is going higher because of tariffs. For now, these companies are keeping prices low.

But at what point do companies need to move into margin preservation mode and raise prices, or even do things like cut costs and let go of staff?

It takes 2 to 3 months to see the actual ramifications of higher tariffs, so we are expecting lower earnings growth in Q3. And when you listen to what CEOs are telling us, how they’re combating higher input costs, they’re leveraging technology and utilizing AI to create some efficiencies. They’re going to be aggressively negotiating with their suppliers, and they’re trying to upskill their labor force. So, we’ve got 7.4 million job openings; however, employers are expected to be very selective in who they hire.

They need that greater productivity. And so, we wouldn’t be surprised if we’re in a slow to hire, slow to fire environment where there are jobs available. But you have to have the skill set match to actually get hired.

Brooke, Forbes* has rated you among the top female wealth managers, among the best wealth managers in the state for, like, the last five years in a row.

How are your clients doing right now? Obviously, risk assets are at an all-time high no matter where you look, but uncertainty is up there, as well. So, are they spending? Are they buying properties or are they buying real estate or what are they doing?

They are. If you look at high-net-worth individuals, they’re continuing to spend, and it’s really the low-income households who really have been hurt.

It’s interesting though, right now when we look at CPI, and you look at the breakdown of what continues to be elevated versus what isn’t. If you look at headline CPI, energy actually had a tick down over the last year. Food prices are flat over the last year, which doesn’t mean it’s not a little bit difficult to, at the cash register at the grocery store, to pay that bill.

However, we aren’t continuing to see that increase. We just are still feeling the pain of inflation impacts over the last few years. However, shelter is the biggest component of CPI, and it makes up about a third of CPI and it continues to be elevated. I think the shelter component was up about 3.7% year-over-year.

However, it’s based on rents and owner-equivalent rent, not the price of your house. So, those that were fortunate enough to buy a home and lock in a 3% mortgage rate and who don’t plan to move aren’t being impacted by that component. So, the high-net-worth individuals are feeling pretty good right now and they’re continuing to spend.

We’re going to get another read on inflation this Friday when we get PCE data at 8:30 a.m. ET. Brooke, we’re going to have to leave things there. Thank you so much for joining us. That is Evans May Wealth managing partner Brooke May.

*Forbes Top Women Wealth Advisors Best-In-State (2018, 2019, 2022, 2023, 2024, 2025), created by SHOOK Research. Most recently presented Feb 2025 based on data gathered from 9/30/23 – 9/30/24. No fee was paid to be included in the ranking. Not indicative of advisor’s future performance. Your experience may vary.