Cheers to 2023! We survived a brutal 2022 where both bonds and stocks fell into bear territory, and we are eager to start a new chapter. With Federal Reserve rate hikes expected to ease mid-year, we see a light at the end of the tunnel. Will the early positive momentum we’ve seen this year continue, or will we have choppy waters ahead? Likely a combination of both, and the name of the game remains patience.

Inflation continues to be the focus as we begin the new year. The Consumer Price Index (CPI) report (i.e., a measure of inflation) released January 12th came in as expected, marking the sixth consecutive decline in CPI. Although CPI is still elevated at 6.5% on a year-over-year basis, it does appear to have peaked, and the market rallied on this news. The Federal Reserve’s (Fed) most aggressive rate hikes in history seem to be tackling inflation as hoped.

Where is the Fed headed with rates this year? The market anticipates a 25-basis point (0.25%) interest rate hike on February 1st, and another 25-basis point (0.25%) rate hike during the March 22nd Fed meeting [1]. This would bring the Fed Funds Rate target range to 4.75% to 5.00%, a level not seen since 2007. The market expects this to be the peak Fed Funds Rate target range.

We expect inflation to continue to come down over the coming months and quarters as a result of continued interest rate hikes. No members of the Fed forecast a cut in rates this year, and most Fed Governors forecast a terminal rate above 5%, which is a disconnect from market expectations. Importantly, until the Fed signals peak rates and a cessation of rate hikes, we believe the market will remain volatile. However, we expect the market will rally once we have clarity on peak rates and the timing of reducing interest rates.

Throughout 2022, corporate earnings surprised on the upside each quarter, so we are paying particularly close attention this year. We believe 2022 Q4 earnings and 2023 Q1 earnings results will be worse than prior quarters. Analysts also project forward-looking guidance to be worse than prior quarters, given continued uncertainties around inflation and interest rates.

FactSet reports that over the past few weeks, earnings expectations for the first and second quarters of 2023 switched from year-over-year growth to year-over-year declines. Specifically, estimated earnings decline for Q1 2023 is negative 0.6%, and the estimated earnings decline for Q2 2023 is negative 0.7% [2].

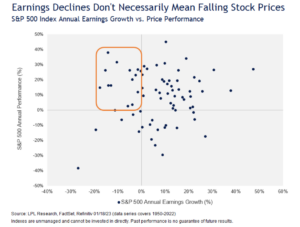

With that said, flat or negative earnings growth does not necessarily mean the stock market will decline. In fact, since 1970, of the 12 years that saw earnings decline for the S&P 500, just 4 of those years were accompanied by falling stock prices [3].

This may seem counterintuitive to many. But remember, the stock market is forward-looking and the market generally prices in earnings declines well in advance – sometimes two or three quarters ahead.

So where do we think the market is headed this year? After the pullback in December, the S&P 500 started the year by rallying and pushed above the 200-day moving average, climbing to over 4,000 points. This is a good technical sign.

Equities remain oversold and we would not be surprised if we tested the lows (near 3,500) from October 2022. But it all goes back to the Fed and rate hikes: when they ease, we expect the market to stabilize and rally. If we see a bottom in early 2023, the chance of double-digit equity returns by year-end is high.

This week will be jammed with important economic data releases, but we will keep an eye on 4Q 2022 GDP and the Fed’s favorite inflation measure: the Personal Consumption Expenditures (PCE) index. PCE will be an important data point as the Fed will be deciding on its next interest rate (the 25-basis point expectation noted above). Importantly, we keep one eye on current data, and one eye on the future. This is how we keep the ship steady as we move through troubled waters. Patiently.

With volatility expected in the short term, how are we preparing and protecting portfolios? As always, we seek to invest in high-quality businesses with hard-to-replicate products and services, sticky revenue models, and strong balance sheets. Never speculative.

The winners of the past won’t necessarily be the winners of the future. We’ve seen a seismic shift from the speculative technology companies that were high flying in 2020-2021, to value-oriented, income-producing companies in the energy, industrials, materials, and healthcare sectors. Bond yields are the most attractive we have seen in years, and we are revisiting allocations, particularly for income-seeking investors.

Looking ahead into 2023, we’re excited to continue our quarterly webinar series to provide more value and educational content to our clients. Be on the lookout for our new Evans May Wealth newsletter this year as well! We have several exciting events planned for the year and we will be sharing details soon about a market update event and webinar with Mary Ann Bartels, Chief Investment Strategist for Sanctuary Wealth.

We look forward to serving our clients and their families in the year ahead. We wish you good health, happiness, and prosperity in 2023!

Read our written commentary here.

Sources:

- CME Fed Watch Tool, as of January 23, 2023.

- FactSet, “S&P 500 Now Projected to Report Year-Over-Year Earnings Declines in Q1 2023 and Q2 2023. January 18, 2023.

- LPL Research, “Earnings Down, Stocks Up? Not as Uncommon as You Think”. January 19, 2023.